The healthcare real estate lending market has been on an upswing in recent years. The COVID-19 pandemic accelerated the shift from hospital inpatient care to patients receiving most of their treatment in outpatient clinics, such as ambulatory care settings, urgent care centers and medical office buildings housed by physician groups. Demographic tailwinds and emerging value-based care reimbursement models have also pushed the industry to outpatient settings.

In JLL’s 2022 Healthcare and Medical Office Perspective research report, the firm wrote that “the fundamentals of population demand for healthcare services, even in times of economic uncertainty, translate into steady real estate demand and investor interest in medical office properties.” Simply put, providing services in a medical office building or outpatient clinic is much cheaper than in a hospital, and the M&A numbers underscore these trends. The healthcare real estate market was one of the key verticals in 2022 that pushed annual healthcare deal volume to a record high of more than 2,400 transactions.

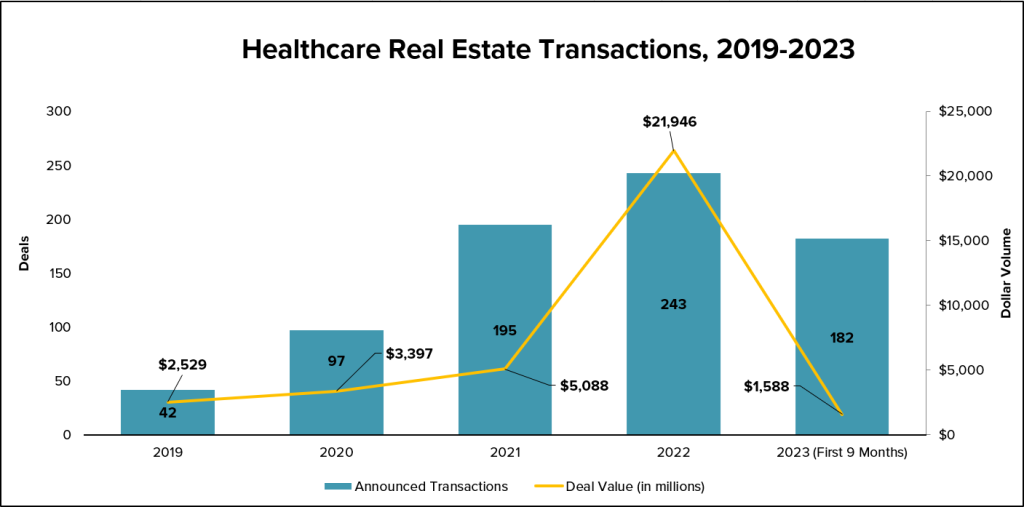

The healthcare real estate sectors’ M&A activity has been rising steadily over the past few years, too, with a surge in 2022 in both deal volume and announced transaction value. There were several very active buyers in 2022 that helped push up activity, including Montecito Medical Real Estate (43 deals), Anchor Health Properties (14 deals), JLL Income Property Trust (six deals) and Welltower, Inc. (five deals). Whereas, the significant jump in deal value can be attributed to the acquisition of Healthcare Trust of America, Inc. by Healthcare Realty Trust. The deal was valued at $18 billion, creating one of the market’s largest pure-play medical office building REITs. So, the decrease to $1.59 billion in spending in the first nine months of 2023 is less dramatic when that deal is removed. However, at an annualized rate, the dollar volume for 2023 is expected to be the lowest for these healthcare real estate transactions since 2018.

The industry (and economy overall) faces severe macro-headwinds, especially regarding interest rates and the lending market. As of September 30, the Federal Interest Rate is hovering around 5.25%-5.50%, taking a significant hit on deal-making across many industries, including health care.

“Because of high interest rates, it is harder to pencil deals for both the originator and the borrower,” said John Nero, who serves as Senior Managing Director of Newmark’s Healthcare Capital Markets Group. As part of his role, Nero leads the debt capital markets initiative for the healthcare capital markets practice, specializing in acquisition, construction and refinancing facilities for borrowers in the healthcare sector, often within the medical office buildings space.

This primer will explore how we ended up in a contracted lending and investment market, what investors can do to navigate it, how the capital markets have already affected M&A activity, where investors can find opportunities, and what 2024 and beyond will look like.

The Fall of SVB and Increased Caution

To understand the current healthcare real estate market and lending environment, we need to discuss the collapse of Silicon Valley Bank (SVB). In short, rising interest rates as a result of inflation caused the value of SVB’s bond portfolio to drop precipitously, so that when depositors tried to withdraw their money from the bank, SVB incurred huge losses when it had to sell off its bonds to cover the withdrawals. When SVB tried to issue their own bonds on the open market to quickly raise money, that generated more panic among its depositors, leading to a final run on the bank and its eventual collapse. This event had a major ripple effect on the lending market and banks, forcing them to contract, as well.

The Federal Reserve’s review of the SVB collapse has pushed the agency to review capital and liquidity requirements for mid-sized banks (over $100 billion in assets) while revisiting how the agency assesses the risk of uninsured deposits and its handling of growing banks transitioning between size classes. The stricter scrutiny, rising interest rates and inflation have all forced lenders to slow down, and these headwinds hit the real estate market in 2023.

“Regional bank lending for commercial real estate became more cautious and conservative in 2023,” said Nero. “However, offsetting that pullback was a more active middle-market and national healthcare lender pool, which helped maintain liquidity in the medical office sector. Debt funds and life insurance companies have also grown interest in the sector.”

Sarah Anderson, who serves as the Senior Managing Director, Health & Alternative Real Estate Assets at Newmark, added her insight.

“When the Federal Reserve stepped in to curb inflation by raising the fed funds rate to over 5%, which was up from virtually 0% in 2021, the aftermath resulted in the failure of several regional banks including SVB and Signature Bank,” Anderson said. “Regional banks need deposits in order to issue new loans, so without a strong base of deposits they aren’t able to lend. This led regional banks to hold onto liquidity, request deposits from their banking clients and not originate as many commercial real estate loans in 2023.”

Unlike seniors housing, which relies on Fannie Mae and Freddie Mac for permanent mortgages, the healthcare real estate market heavily depends on bank loans. Approximately 89% of medical office building loans originated in banks in 2022, up from 2021 with 85%.

“Overall risk tolerance for real estate lending is low from banks and regulators across all asset classes right now,” said Nero. “Fortunately, medical office buildings are generally viewed as a safe haven and stable asset class compared to other collateral.”

What now for the healthcare real estate market?

Although the macroeconomic headwinds are steep, that is not to say closing a loan is impossible, especially in the healthcare real estate market. After all, medical office buildings and healthcare real estate assets have proven to be a recession-resistant asset class. During the height of the COVID-19 pandemic in 2020, medical office buildings had the highest rent collection rate in all medical real estate. According to research by JLL, in 2020, asking rates for triple-net lease payments for medical office buildings averaged just below $22 per square foot nationally, which steadily increased each quarter to $23 per square foot in Q2:22. That was the 11th quarter in a row with an average medical office building rent increase.

Nonetheless, investors need to be mindful of the market environment. Firstly, despite the high cost of debt and acquisition financing, buying is still the better route than constructing a new property since development costs have skyrocketed, from materials to labor. Research completed by the Turner Construction Company, a North America-based, international construction services company, found another increase in construction costs in the second quarter of 2023, a 1.19% quarterly increase from Q4:22 and a 6.39% yearly increase from Q2:22. This is after a staggering rise in development and material prices in 2022 due to inflation and supply chain difficulties.

With all of this uncertainty surrounding costs, lenders have a few critical criteria when considering a loan for a medical office building, such as an emphasis on what lease maturities are in place. They are more comfortable if investors can demonstrate five years of weighted average lease term across the building.

In early 2023, Big Sky Medical Real Estate worked with JLL to secure $190 million in acquisition financing for ten healthcare properties totaling 857,779 square feet. The terms include a five-year, floating-rate loan from a bank syndicate led by Capital One Healthcare. The properties, which are collectively 87% occupied, serve a wide range of healthcare uses, including outpatient medical office buildings, ambulatory surgery centers, diagnostic imaging centers and more. The tenants were some noteworthy providers, including Texas A&M Health Science Center.

Since regional banks have stepped back from the market (mostly), investors and borrowers will have better odds with larger national banks. Institutions such as Capital One Healthcare, BMO Bank, First Citizens Bank and Fifth Third Bank are some lenders worth highlighting.

“You also want to make sure the lenders have a dedicated practice of professionals that are focused on MOB lending and other healthcare real state and understand the nuances of the asset class,” Nero said.

In September 2023, Flagship Healthcare Propertiesacquired a 38,786-square-foot medical office building and ambulatory surgery center in Fredericksburg, Virginia, and Fifth Third Bank provided the acquisition financing for this deal.

In August 2023, a joint venture led by Rethink Healthcare Real Estate received $50.3 million in refinancing for Medical Pavilion at White Oak, a 169,000-square-foot medical office building in Silver Spring, Maryland. First Citizens Bank, through its Healthcare Finance division, provided the financing.

“Larger national banks are the ones that are carrying the market right now,” Nero said.

Alternative Assets

There are also market tailwinds that make alternative assets an attractive buy, such as inpatient behavioral health hospitals or inpatient rehabilitation facilities. Demand for mental health care services and substance use disorder treatment have surged in recent years. In late 2021, Sabra Health Care REIT, which has a significant stake in the long-term care sector but has started diversifying into behavioral health care,provided Recovery Centers of America (RCA) with a $325 million mortgage loan secured by eight inpatient addiction treatment facilities. The loan bears a yearly interest at 7.5%, has an initial five-year term and gives Sabra a right of first offer to acquire the underlying facilities should RCA decide to sell any of the eight centers.

“Behavioral healthcare facilities and inpatient rehabilitation hospitals present interesting opportunities for investors and lenders in this market,” said Nero. “We are seeing an increased demand from capital given the macro tailwinds and favorable reimbursement patterns.”

Following that announcement, Sabra said in its Q2:22 earnings call it will invest $800 million in behavioral health and begin converting some of its senior care properties into behavioral health properties. And Sabra is not the only investor focused on conversions, which could be an easier ask in the lending market.

In July 2022, H2C Securities Inc. served as the exclusive advisor to AM Behavioral Health, LLC, a joint venture between the principals of Meridian Senior Living, LLC and Midwest Behavioral Management, LLC, to secure a $30.4 million equity and debt placement for the conversion of a senior living community to a 96-bed behavioral healthcare facility in the Dayton, Ohio, market.

The parties didn’t provide specific lending terms, but H2C did state that the joint-venture equity was provided by a Texas-based real estate private equity firm with a demonstrated track record in the healthcare sector. And they were joined by Ohio-based bank with a presence across four states to complete the financing.

“These types of facilities are pretty specialized, so investors are seeing a lot of positive attributes because hospitals are referring a lot of patients to those settings,” said Nero.

“Survive until ’25”

“The mantra in the market right now is ‘Survive until ‘25’,” said Anderson, which does not bode well for M&A activity in 2024.

There is a lot of uncertainty surrounding the 2024 healthcare real estate and lending market. Much of it will depend on the Federal Reserve and how it handles the eventual decline in interest rates. The most likely scenario is that interest rates, however, will remain at elevated levels throughout the year due to the persistent inflation that has embedded itself in the economy after so many years of low interest rates. So, for many, the best course of action is to weather 2024 until the debt markets are expected to loosen in 2025.

“Investors and lenders don’t even need to see a pullback or a rate cut,” said Nero. “The biggest thing the industry needs is stability in interest rates.”

Anderson also noted another upcoming issue in 2024: loans maturing. “Originations in 2023 are far below what we saw in 2022,” said Anderson. “And with over $500 billion of senior commercial real estate debt set to mature in 2024 ($250 billion of which is multifamily), something has to happen.” On top of this, there are $1 trillion total in commercial mortgages maturing in the next two years.

Any distress resulting from these maturities would lead bank credit committees to be even more cautious in approving new loans, decreasing leverage, making terms more stringent and overall increasing the cost of capital to borrowers. That is especially true if interest rates remain elevated. Healthcare M&A and new development activity would almost certainly take a hit. But even with all the headwinds on the horizon, no one is predicting a total capital freeze in this sector. Healthcare real estate properties, unlike other types of commercial real estate, fill a necessary service, and as outpatient services continue to surge, that need will only grow, even if investor returns are reduced.

Dylan Sammut is a Healthcare Editor for Levin Associates.

Levin Associates provides comprehensive coverage of the deals, companies, and trends shaping the healthcare industry. Clients have access to proprietary M&A transaction data and daily news & analysis through the LevinPro platform.

Schedule a demo today to see what LevinPro can do for your team.

Schedule a demo

Gain access to the best healthcare and long-term care investment intelligence, data, and analysis.